Global equity markets delivered mixed performance over the week as investors digested central bank decisions, economic data and political developments across major regions.

United States

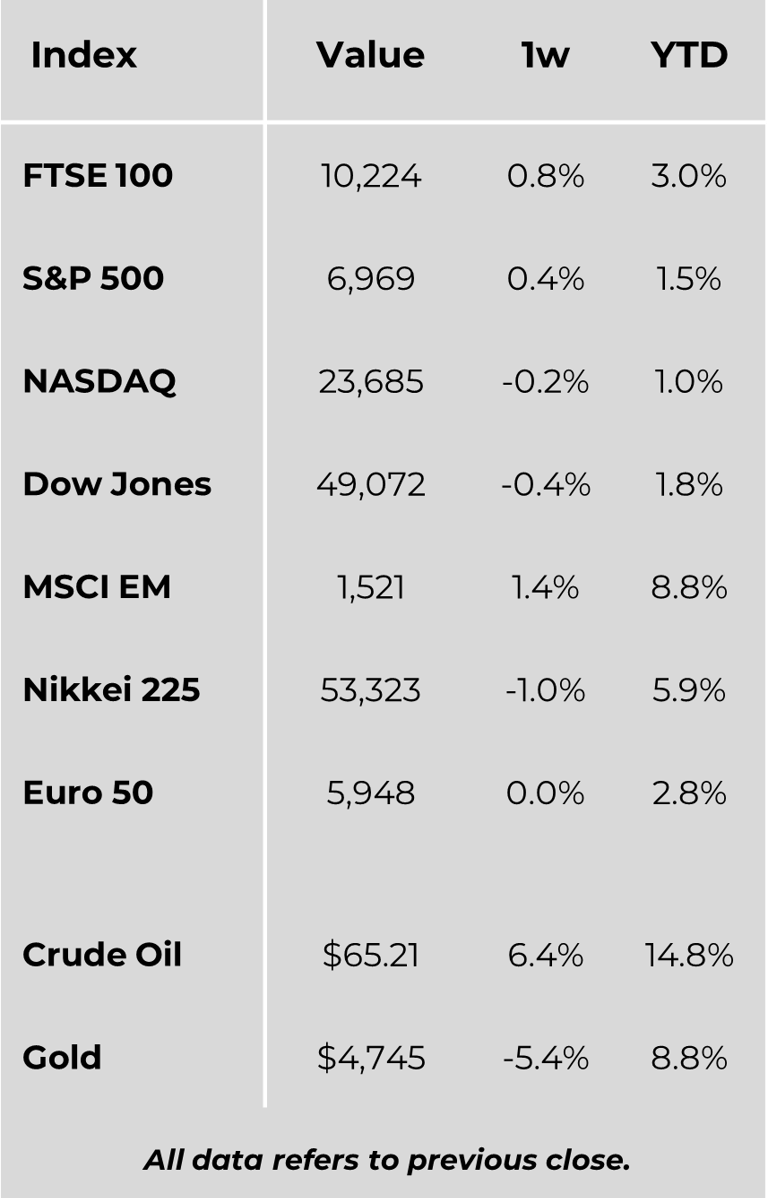

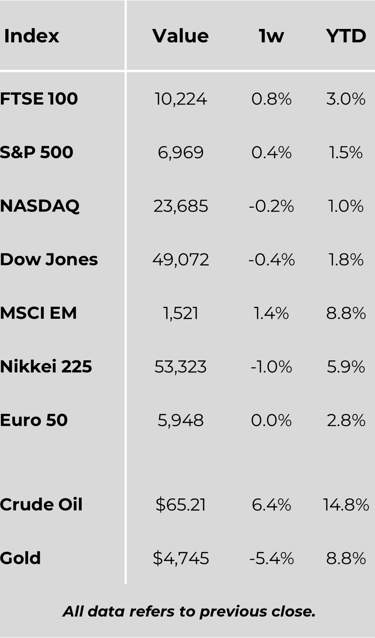

The S&P 500 Index rose during the week, briefly surpassing the 7,000 mark before retreating from its intraday high. Large-cap value stocks outperformed growth peers, while small- and mid-cap stocks ended lower. Sector performance was led by communication services and energy, with healthcare underperforming. Economic data was mixed: consumer confidence dropped sharply to 84.5, the lowest since May 2014, reflecting weaker sentiment on both the economy and labour market. Meanwhile, initial jobless claims were little changed at 209,000, and continuing claims fell to 1.83 million, the lowest since September 2024. The Federal Reserve left the benchmark interest rate unchanged at 3.5%–3.8%, noting that economic activity remained solid and inflation “somewhat elevated.” Fed Chair Jerome Powell highlighted that rates did not appear “significantly restrictive,” signalling a meeting-by-meeting approach to future adjustments. Separately, President Trump nominated former Fed governor Kevin Warsh as the next Fed Chair, pending Senate confirmation.

Europe

The STOXX Europe 600 Index gained 0.4% in local currency terms, supported by corporate earnings optimism. Major markets were mixed: Italy’s FTSE MIB rose 1.6%, the UK’s FTSE 100 added 0.8%, while Germany’s DAX fell 1.5% and France’s CAC 40 declined 0.2%. Eurozone GDP growth for 2025 came in at 1.5%, exceeding expectations, with stronger investment, consumption, and exports driving output. The European Commission’s sentiment indicator rose to 98.2 in January, signalling broadly improving confidence, particularly in France. Germany, however, trimmed its growth forecast to 1.0% for 2026 due to slower implementation of economic and fiscal measures. In the UK, mortgage approvals fell to 61,013 in December, the lowest in 18 months, reflecting ongoing housing market pressures.

Japan

Japanese equities declined, with the Nikkei 225 down 1% and the TOPIX falling 1.8%, weighed by technology sector concerns and a stronger yen affecting export earnings. Core Tokyo inflation eased to 2% year-on-year in January, below expectations, limiting pressure on the Bank of Japan for further tightening. Political uncertainty ahead of the lower house elections also contributed to yen volatility.

China

Chinese onshore markets were mostly flat, while the Hang Seng rose 2.4%. Thirteen out of twenty Chinese provinces lowered their 2026 GDP growth targets, reflecting a cautious outlook despite government support measures.

Other Key Markets

Hungary’s central bank kept interest rates steady at 6.5%, noting balanced inflation risks and gradual easing in labour market pressures. Brazil also left its Selic rate unchanged at 15%, though policymakers suggested that gradual rate cuts could begin if inflation continues to improve. Both central banks emphasised a careful approach amid domestic and global uncertainties.

Major Company News:

Europe’s largest oil firms - Shell, BP, TotalEnergies, Eni, Equinor - plan to cut shareholder payouts by 10% to 25%, focusing on buybacks amid lower oil prices and balance sheet preservation.

Ikea closes seven large Chinese stores, shifting to smaller formats as consumer demand struggles amid a prolonged property slowdown, reflecting a broader “store network optimisation” strategy.

Starling Bank aims to sell its Engine software to US lenders, targeting outdated systems and growth opportunities, with Deloitte and PwC advising on client acquisition in North America.

Investor Michael Flacks eyes British Steel, planning to combine it with a distressed Italian plant, seeking to electrify production and create one of Europe’s largest integrated metals groups.

Weekly Update

2nd February 2026

Markets Data

This publication is intended to be Hexagon Wealth’s own commentary on markets for clients. Hexagon Wealth Limited is authorised and regulated by the Financial Conduct Authority. FCA number 483403. Hexagon Wealth Limited is registered in England and Wales under company number 04503414. Whilst Hexagon Wealth uses reasonable efforts to obtain information from sources which it believes to be reliable, it makes no representation that the information or opinions contained in this document are accurate, reliable or complete and will not be liable for any errors, nor for any actions taken in reliance thereon. Such information and opinions are subject to change without notice. We expect readers to rely on their personal views on the subject when reading the opinions expressed above and contact their financial adviser before taking any action. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice please contact your financial adviser.